STRATEGY [TL;OR]

The strategies employed by our systems have been in development for over 8 years and tested on many trading platforms. While we cannot guarantee profits, we can say that every effort has been made to create a stable, reliable technology that can run autonomously for long periods with reduced human intervention. It is our belief that someday in the near future (should humans survive) conventional retirement accounts and other forms of investing will become fully automated. That is to say, run by a robot. This process is well underway today as evidenced by the sheer number of expert advisers, Pine scripts, Ninja scripts and robotic networks in use by professional trading organizations. The following is an overview of how our strategies make trades in your account.

How does the strategy work?

All of our systems implement one or a combination the following market entry methods:

-

Trend follow

-

Swing trader

-

Linear price pressure

How they are implemented in a system has a lot to do with the effect we are trying to achieve. Hedging systems gain or lose based on being long and short on the same symbol simultaneously within the same account. In theory, one side closes at a profit then the other side when the market retraces. To achieve such a condition, we assign two strategies at different bar intervals to the same symbol. The first strategy is a swing entry type and the second a trend (or vice versa). A good example is Majestic Hedge. This system employs three symbols and six strategies. Each instrument having a swing trader and trend follower managing its market entry end exit points. On Majestic Hedge a 15 minute ping pong strategy continuously looks for swing entry conditions while a 5 minute trend follow strategy checks for trending prices. What you will see in your account is two separate set of trades existing independently on the same symbol. While the intent is to have both sides in opposing trade directions, they often do align. In this case you may see a large single direction trade eating up some account margin. Opposing or not, both sides are traded according to the rules of its designated trading method (swing or trend).

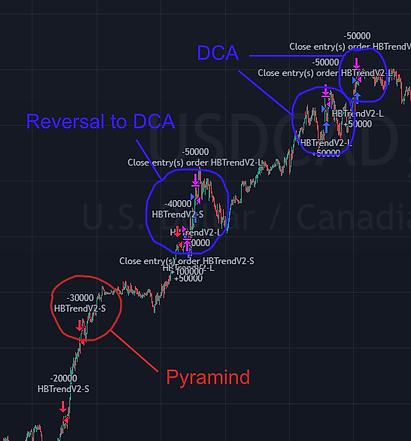

In the aforementioned configuration, the 5 minute strategy will reverse when the trend looks to have changed direction. Your account will take a loss when that happens. Meanwhile, the 15 minute will likely draw down in its current direction. Needless to say, choppy markets are not your friend with the 5 minute strategy. Ideally, losses are made up by the 15 minute on the rebound chop. When both sides are aligned with the MFE bias, the 5 minute strategy will take profit often and independent of the 15 minute strategy. What you will see in the account is entry and exits while the price moves favorably. Conversely, should the market crash and the 15 minute be wrong footed, you will see pyramid trades added to the symbol in the MAE direction. In this case, straight up trend reversals are not your friend with the 15 minute strategy. When a symbol is weighted with pyramid trades the strategy will exit the trade early (bale out) should the price recover sufficiently. It should be mentioned that most of the profit (if any) made by our systems will be the result of pyramiding trades. If you are not comfortable with this style of trading then our systems may not be for you. To be sure martingale strategies are widely panned in trading circles and really get a lot of bad press.

Not your old school DCA

DCA (Dollar-cost averaging)

Similar to Pyramids, DCA is another form of Martingale trading. However, only entry trades are increased and only at the onset of the position. Trades that have closed at a loss increase the debt accumulator and debt sequence counter. Each strategy keeps track of all its losses and attempts to recover those losses through the DCA (dollar-cost averaging) facility. Each losing trade increases the loss counter by one and the next open trade size is made larger by a multiple of this value. Specifically, the loss count plus one times the base size equals the next open amount. (((n + 1) x base size) = next size). Each winning trade reduces the debt by its gain amount. Once the debt is sufficiently recovered, the trade size returns to normal (i.e. the strategy base size). In addition to the incrementing debt sequence number, all strategies employ a reversal offset. Here is how this feature works: When a trade hits the stop, the trade direction is reversed but at a multiple of the base size times 5 (parameter value).

So a stopped out short with a 0.01 base size will produce a long of size 0.05. The position will remain elevated until a numeric threshold is reached which can be between 50 - 200 pips. At which point the trade size will return to the debt sequence size or normal if the metered debt is recovered. Though the use of DCA in this manner is intended as a debt recovery mechanism, a bad run of consecutive losses can quickly cascade into an avalanche of increasingly larger losses. Also the debt recovery system is not designed to recoup account currency losses only pip losses as measured from the entry trade. Please keep this in mind when determining starting capital and base trade sizes. Remember, you should only be trading what you can, realistically, afford to lose.

Do you believe in overbought?

Swing Trading

Referred to by various names; Swing trading, range trading, support and resistance all describe the notion of a price being too high or too low. In trading parlance too high is said to be meeting resistance while too low is hitting support. This concept forms the basis of the trading discipline where a short position is taken at overbought levels and a long at oversold. When depicting such levels on the chart the area between overbought and oversold becomes the trade-able area know as the range. It is important to understand that this is merely a trading methodology. No actual price boundary truly exists other than zero. Our Ping Pong strategy functions as a support and resistance trader. Using proprietary algorithms to determine a range, short positions are entered at tops and long positions

at bottoms. The actual sequence involves positions reversals so what you will see on the chart (under ideal conditions) is a short converted to a long when it falls to oversold and a long converted to a short after rising to overbought. Ticket numbers are treated differently by MetaTrader 5 between hedging and netting accounts when reversals occur. It’s just something to be aware of when examining the trade log.

Fundamentally, swing trading is flawed as trades are placed counter to prevailing price pressure. This typically results in increased drawdown amounts per trade since overbought and oversold levels may stay that way for some time. We have spent many years developing range detection algorithms and improving our Ping Pong strategy. Our best design uses multiple time frames to measure price action. Once the strategy discerns the range a pivot point matrix is created which maps out possible points where a reversal may occur. We use a Z-Score Mean Reversion indicator to measure the range against a higher time frame trend line. The actual entry setups are complex but are best described as a Klinger oscillator histogram operating with higher time frame EMAs. Position exits are simply the opposite entry signal. So a long will exit on the next Klinger short and vice versa. Because Ping Pong is a counter trade strategy, it spends most of the time waiting for the market to pivot back to the mean. While waiting, the position typically draws down. Subsequently, the strategy will add pyramid trades in the MAE space. We like to mash up the Ping Pong with a trend follow strategy on the same symbol to produce a better balance on hedging accounts. This way one strategy is more likely to align with price pressure while the other opposes it. The expected outcome in this scenario is for both sides to close favorable though at different times (incongruent).

CFTC RULE 4.41 - Hypothetical or simulated performance results have certain limitations. Unlike an actual performance record, simulated results do not represent actual trading. Also, since the trades have not been executed, the results may have under — or over — compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profit or losses similar to those shown.